Mortgage Calculator

Recent Articles

What Is a Mortgage?

Mortgage is a loan for the purchase of a house. Most people do not have enough money to pay for a house within one tenure, and so they take an entire bank or lender loan that they are repaying monthly for many years.

Important: House by bank can be taken or lender, once someone stops payments.

What Are Mortgage Payments?

Every month, you pay a little on:

Principal

That's what you borrowed.

Interest

The bank charges you for the money it lends you.

Taxes & Insurance

These are additional costs for property taxes and home insurance (sometime included).

Example:

You buy a house worth $300,000 and borrow $240,000 from the bank.

Your monthly payment is:

- ✔️ Some of that $240,000 loan.

- ✔️ Interest the bank charged on it.

- ✔️ Property taxes and insurance if included.

Important Mortgage Terms

Down Payment

The money you pay upfront on the purchase of a house.

- • Typically around 20% of the home price, but in some cases, as little as 3%.

- • If you pay less than 20%, you're required to pay extra insurance (PMI).

Example for a $300,000 home:

✔️ 20% down = $60,000 upfront

✔️ 10% down = $30,000 upfront

Loan Term

The number of years it takes you to pay the loan back.

30 and 15 years are the two most common options.

30-year loan

✔️ 30-year loan = Lower monthly payments, but more total interest.

15-year loan

✔️ 15-year loan = Higher monthly payments, but total interest less.

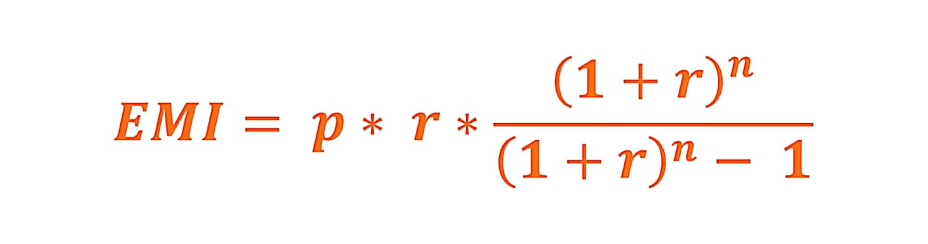

Example: $240,000 loan at 5%

✔️ 30 years → $1,288 per month, $215,000 in total interest

✔️ 15 years → $1,898 per month, $94,000 in total interest

Interest Rate

The percentage charged by the bank against the loan.

The smaller the number, the smaller the money you will pay as the year goes by.

Example: 5% interest rate on $240,000 means $12,000 a year in interest in the early years.

Fixed Rate

The rate remains unchanged for the term of the loan.

Adjustable Rate

The rate may vary after 5 years or so.

Extra Costs

Property Taxes

Taxes on your home payable to the government.

Typically 1% of the value of the house per year.

Example:

For a $300,000 home property tax = $3,000 a year or $250 monthly.

Home Insurance

To cover your home for fire, storm, and all other damages.

Costs $800-$2,000 a year.

PMI (Private Mortgage Insurance)

If you pay less than 20% down, you have to pay additional insurance or PMI.

When you pay off 20% of the homes value you are eligible to cancel PMI.

Example:

PMI for a home worth $300,000 may be $100-$300 each month.

HOA Fees

Some neighborhoods or condos charge fees on a monthly basis for maintenance.

Can be $50-$500 per month.

For more info - Check Types of Home Loans section below

Types of Home Loans

Conventional Loan

- ✔️For those with good credit and intending to put 20% down.

- ✔️PMI free with 20% down.

FHA Loan (Government-Backed)

- ✔️Minimum down payment of only 3.5%.

- ✔️Best for those with low credit scores.

- ✔️Mortgage insurance is required for the entire loan.

VA Loan (For Military and Veterans)

- ✔️Zero down payment.

- ✔️No PMI.

USDA Loan (For Rural Homes)

- ✔️Zero down payment.

- ✔️Meant for low-income buyers in rural areas.

Jumbo Loan (Very Expensive House)

- ✔️For homes that cost more than normal loan limits.

- ✔️Requires good credit and a large down payment.

How To Pay Off Your Mortgage Faster

Extra Payments

Paying above the minimum every month helps pay off the loan quicker.

Example:

Paying an additional $200 a month can save you about $50,000 in interest.

Biweekly Payments

Instead of one monthly payment, pay half every two weeks.

So, it adds an extra payment each year that will help pay off the loan quicker.

Example:

A $1,200 monthly payment becomes $600 every two weeks, adding one extra payment each year against the loan.

Refinancing

Replace your old loan with a new one at a lower interest.

It is also possible to reduce the term of loan (30 to 15 years).

Example: Previously loaned at a rate of 6% but refinancing at 4%, our payments drop and we save considerably on interest.

Final Tips

- ✔️ Choose the right loan for your situation.

- ✔️ Understand all additional costs.

- ✔️ Pay extra whenever possible to save on interest.